BSP Circular 808, Series of 2013, and its subsequent Information Technology Risk Management (ITRM) framework updates require every supervised Philippine financial institution to maintain auditable, secure, and recoverable communications infrastructure. That single regulatory reality has turned legacy telephone system replacement from an IT wish-list item into a board-level compliance obligation for banks operating across Metro Manila, Cebu, Davao, and provincial branches. If your bank still runs proprietary PBX hardware at each site with siloed trunk lines and no centralized call recording, you’re carrying compliance risk that gets harder to defend with every BSP examination cycle.

This playbook walks through the chronological phases of a financial services VoIP migration for multi-office Philippine banks, from initial audit through production rollout, in the order that decisions actually need to happen.

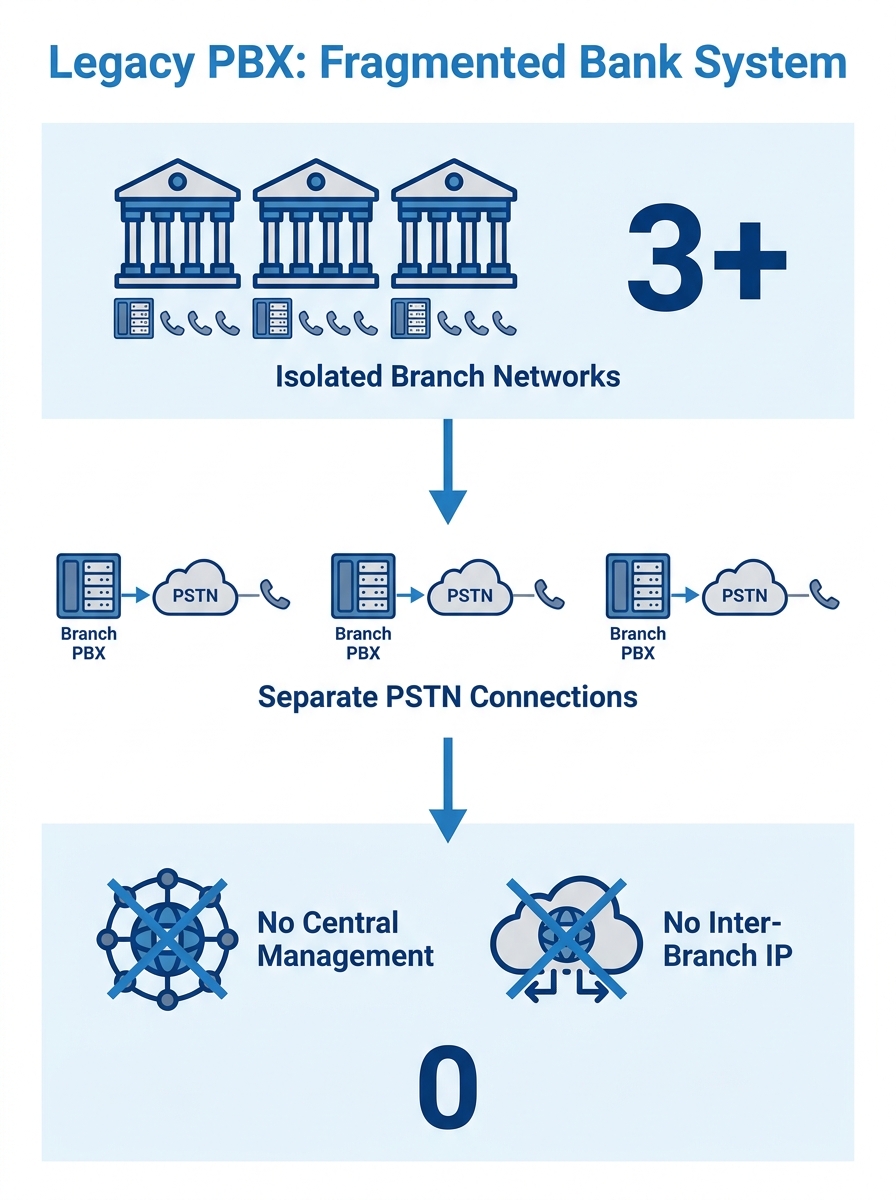

Analog Lines, Proprietary Hardware, and Thirty Branches

The typical mid-size Philippine bank operates between 15 and 80 branches, each equipped with its own PBX or key telephone system purchased independently over the past 10 to 20 years. You’ll find Panasonic KX-series units in provincial branches, NEC or Avaya systems in the head office, and the occasional Cisco CallManager deployment at a regional hub. These systems don’t talk to each other. Inter-branch calls route through the PSTN, billing accumulates on separate PLDT or Globe accounts per site, and nobody at the IT department has a unified view of call volume, call quality, or even how many active extensions exist across the organization.

This fragmentation creates three problems that compound over time. First, maintenance costs escalate because each PBX model requires its own spare parts inventory and vendor support contract. Second, compliance gaps widen because call recording, if it exists at all, lives on local storage with no centralized retention or retrieval capability. Third, the bank’s customer service operation can’t scale because adding a new branch means procuring, configuring, and installing yet another standalone system.

When an institution providing secure communications for Philippine banks runs infrastructure this fragmented, the operational risk extends beyond telephony into business continuity and regulatory exposure.

The Full Infrastructure Audit

Before touching any phone system, you need a complete inventory. This sounds obvious, but in practice it’s the step most banks shortchange because it’s tedious. The audit must cover every branch, not just the head office and the two or three locations that IT visits regularly.

Here’s what the inventory needs to capture at each site:

- PBX make, model, and firmware version along with the number of active analog trunk lines and DID numbers

- Extension count versus actual usage, because many branches have 30 provisioned extensions but only 12 people making calls

- Existing network infrastructure including router model, switch capabilities (does it support VLANs and PoE?), and internet bandwidth from each ISP

- Analog dependencies such as fax machines connected to FXS ports, alarm systems using analog lines, and elevator emergency phones

- Call recording status, specifically whether recordings exist, where they’re stored, and how long they’re retained

The audit almost always reveals surprises. Branches in Visayas and Mindanao frequently run on 5 to 10 Mbps DSL connections that can’t support concurrent voice and data traffic without significant QoS work. Some branches still use rotary-style analog handsets connected through adapter plates. Documenting these realities early prevents the kind of mid-rollout emergencies that stall multi-office PBX consolidation projects for months.

If your IT team hasn’t gone through a structured network assessment before, the checklist we outlined for government VoIP deployments applies equally well to banking environments and covers the baseline measurements you’ll need.

BSP Compliance and What It Demands from Your Phone System

The Bangko Sentral ng Pilipinas doesn’t publish a specific circular about VoIP. What it does publish are the ITRM guidelines within the Manual of Regulations for Banks, which impose requirements on any IT system that handles customer data, supports critical business processes, or connects to third-party service providers. Your phone system touches all three.

IP telephony compliance in the Philippine banking sector means satisfying several concrete requirements:

- Data residency and access controls. Call recordings that capture customer information (account numbers read aloud during verification, personal details confirmed over the phone) fall under data privacy obligations. The system must enforce role-based access so that only authorized personnel can retrieve recordings.

- Business continuity and disaster recovery. The BSP expects supervised institutions to demonstrate that critical systems can survive site failures. A VoIP deployment that runs entirely from a single cloud tenant with no local survivability fails this test. This is where backup and recovery solutions become a non-negotiable part of the architecture, ensuring call data and configuration can be restored after any disruption.

- Third-party risk management. If you use a hosted or cloud PBX provider, the BSP’s outsourcing guidelines apply. Your contract must specify data handling, audit rights, and exit strategies. Google Cloud, for example, explicitly addresses BSP ITRM requirements in its contracts for Philippine regulated entities, and your VoIP vendor should demonstrate equivalent rigor.

- Audit trail and logging. Every call event, configuration change, and administrative action must be logged and retained for the period specified in your bank’s records management policy.

Banks that skip this mapping exercise discover the gaps during BSP examination, which is the worst possible time to learn that your shiny new VoIP platform doesn’t generate the logs that examiners expect.

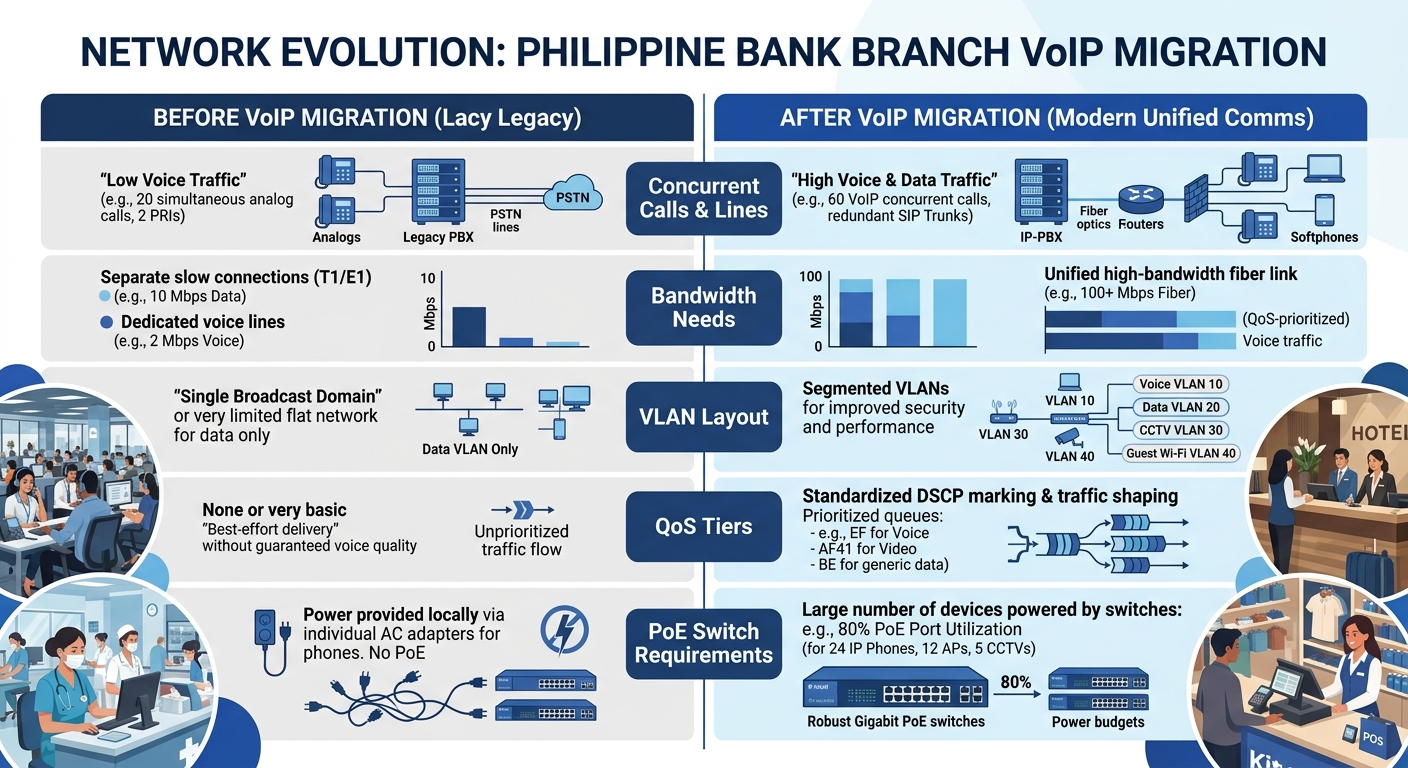

Rebuilding the Network Layer First

You cannot drop IP phones onto the same flat network that handles teller workstations, ATM management traffic, and general internet browsing. Voice traffic is unforgiving of latency, jitter, and packet loss in ways that email and web browsing are not. The network rebuild has to happen before VoIP deployment begins, or you’ll spend the next two years chasing call quality complaints that have nothing to do with the phone system itself.

The core network changes for a banking VoIP environment include:

VLAN segmentation. Voice traffic gets its own VLAN at every branch, isolated from data VLANs and especially from the core banking system network. The rationale goes beyond call quality. Network segmentation limits lateral movement in the event of a breach, which is critical when voice endpoints sit on desks throughout the branch. We’ve written extensively about why unified communications fails without proper network segmentation, and the principle applies with extra force in financial services.

QoS policies on every hop. DSCP markings for voice (EF/46) and signaling (CS3/24) need to be configured on branch switches, WAN routers, and any MPLS or SD-WAN equipment in the path. If your bank uses MPLS from PLDT or Globe for inter-branch connectivity, confirm that your provider honors DSCP markings end-to-end. Many don’t by default.

Bandwidth upgrades where needed. A single G.711 voice call consumes roughly 85 Kbps in each direction with overhead. A branch with 10 concurrent calls needs about 1.7 Mbps of dedicated voice bandwidth. That 5 Mbps DSL line at your Cagayan de Oro branch won’t cut it once you add data traffic on top. Budget for fiber upgrades at branches where the math doesn’t work.

PoE switching. IP phones draw power from the network switch through Power over Ethernet. Replacing non-PoE switches across 30 to 50 branches is a significant line item. Fanvil and Yeastar IP phones typically require 802.3af (Class 2 or 3), so you don’t need high-wattage PoE++ switches, but you do need switches that can deliver 15.4W per port across enough ports for all phones plus a margin for wireless access points.

The network rebuild has to happen before VoIP deployment begins, or you’ll spend the next two years chasing call quality complaints that have nothing to do with the phone system itself.

The Pilot Branch

Pick one branch that represents a realistic test case, not your best-connected head office and not your most remote provincial site. An ideal pilot branch has 15 to 25 staff, a mix of teller and back-office roles, moderate call volume, and a network connection that’s good but not exceptional. A regional branch in Cebu or a mid-tier Metro Manila branch usually fits.

The pilot serves three purposes. It validates your voice quality under real working conditions. It exposes integration issues with your core banking applications, door access systems, or alarm panels that still need analog connectivity. And it gives your IT team a repeatable deployment process before they have to do it 29 more times.

For the pilot deployment, use FXO gateways (Yeastar TA series or equivalent) to bridge any remaining analog lines during the transition period. This lets the branch keep its existing PLDT trunk as a failover path while primary calls route over IP. Don’t rip out analog lines during the pilot. That’s a production rollout decision, not a testing decision.

Run the pilot for three to four weeks. Collect jitter, latency, and packet loss metrics from the IP PBX dashboard continuously, and pair those numbers with structured feedback from branch staff. As we’ve covered in our article on using user feedback as a VoIP diagnostic tool, the quantitative metrics and qualitative complaints don’t always align, and you need both data sets to make sound decisions about proceeding to wider rollout.

Warning: Don’t declare the pilot successful based on the first three days. Call quality problems in banking environments often surface during peak periods like payroll processing days, quarter-end reporting, and month-end reconciliation when data traffic spikes compete with voice.

Branch-by-Branch Rollout Across Regions

After the pilot validates the architecture, the multi-office PBX consolidation proceeds in waves. Group branches by region and network readiness, not by alphabetical order or organizational hierarchy. Branches that already have fiber connectivity and PoE switches go first. Branches that need ISP upgrades and switch replacements go in later waves after those infrastructure changes are completed.

A practical rollout cadence for a 30-branch bank looks like this:

- Wave 1 (weeks 1 through 4 post-pilot): 5 to 7 branches with the strongest network infrastructure. These become reference sites for the remaining waves.

- Wave 2 (weeks 5 through 10): 10 to 12 branches. By this point, your deployment team has a refined process and can handle two branches per week.

- Wave 3 (weeks 11 through 16): Remaining branches including those that required bandwidth upgrades, plus the head office if it wasn’t part of the pilot.

Zero-touch provisioning changes the economics of each wave dramatically. With Yeastar P-Series or similar platforms, you can pre-configure phone profiles at the central site, ship Fanvil or Yealink handsets directly to each branch, and have branch staff plug them in. The phone pulls its configuration from the central server on first boot. No IT technician needs to travel to Tacloban or General Santos for a phone installation.

The lessons from multi-office VoIP integration over public networks are directly relevant here. Branch-to-branch call routing over your WAN connection eliminates PSTN toll charges, but it also means your WAN becomes a single point of failure for inter-branch communications. Every branch needs a local survivability path, either through a local SIP trunk or an analog PSTN fallback via FXO gateway, so that internal branch operations continue even if the WAN link drops.

Modernizing the Banking Contact Center

Banking call center modernization follows a different rhythm than branch telephony replacement. Your contact center handles concentrated call volume with specialized routing requirements: IVR trees for account balance inquiries, skills-based routing to loan officers versus card services versus branch operations, and mandatory call recording with real-time supervisor monitoring.

The contact center migration typically happens as its own phase, either before or after the branch rollout, but rarely during it. The reason is risk management. You don’t want your highest-volume customer touchpoint in transition at the same time your IT team is deploying phones across branches.

A VoIP-based contact center for a Philippine bank should deliver:

- SIP-based trunk connectivity that scales call capacity without adding physical lines. A 50-seat contact center that previously needed three PRI circuits (69 channels) can run on a pair of SIP trunks with automatic failover.

- Call recording with encryption at rest and in transit, stored on infrastructure that meets BSP data residency expectations. This means Philippine-hosted storage or a cloud provider that can demonstrate Philippine data center presence.

- CRM integration through screen pops, so that when a customer calls, the agent immediately sees the account profile. This integration point is where the real productivity gains appear, and it’s something that a traditional PBX system could never deliver because the voice and data worlds were completely separate.

- Real-time and historical reporting that gives operations managers visibility into queue depth, average handle time, abandonment rates, and agent utilization across every shift.

The contact center is also where AI-driven features start to earn their keep. Sentiment analysis on live calls can flag escalation-worthy interactions before a customer complaint becomes a BSP consumer assistance case. Voicemail-to-text transcription reduces callback processing time. These features arrive as software updates on the VoIP platform rather than requiring hardware changes, which means the bank’s contact center capabilities can evolve quarterly instead of waiting for the next capital expenditure cycle.

Where the Numbers Land Today

A 30-branch Philippine bank that completes this migration typically sees PSTN line rental costs drop by 40 to 60 percent, because inter-branch calls no longer transit the public telephone network. Maintenance contracts for legacy PBX hardware, which can run PHP 50,000 to PHP 150,000 per site annually depending on the vendor and system age, consolidate into a single platform support agreement. For a 20-user branch, the monthly savings can reach PHP 40,000 or more when you factor in eliminated trunk lines, reduced maintenance, and lower long-distance charges between branches.

But the compliance story matters more than the cost story for financial institutions. After migration, the bank has centralized call recording with searchable metadata, complete audit trails for every configuration change, role-based access controls enforced at the platform level, and disaster recovery capabilities that satisfy BSP business continuity requirements. These are capabilities that no collection of standalone branch PBX systems can deliver, regardless of how well-maintained they are.

The financial services VoIP migration path for Philippine banks follows the same engineering principles as any multi-site telephony project: audit first, fix the network, pilot carefully, roll out in waves, and treat the contact center as its own workstream. What makes the banking context distinct is the regulatory overlay from BSP and the elevated consequences of getting security, recording, or business continuity wrong. Every architectural decision from VLAN design to vendor selection to call recording retention needs to pass through that compliance filter before it passes through the procurement process.